FOCUS ON FINE JEWELLERY AND WATCHES

VIEWS From THE WealthY CONSUMER

wiediger@unsplash

Survey Background

This report updates purchasing trends and sentiments on luxury watches and fine jewellery. The survey was completed by 100 respondents in each of the UK, US and China in April 2022, and was balanced 46:54 in terms of male:female and 55:45 for under-45s vs over-45s. When converted to USD, the sample had a high median HHI of almost $475,000.

Key Findings

Among the plethora of fine jewellery brands, Cartier is comfortably the most widely cited top-of-mind. 43% of the total sample listed it as the brand which came to mind first, with equally high mentions across all three countries. Tiffany is another strong performer, with almost one in five respondents listing it as the fine jewellery brand which came to mind first.

- One brand also dominates the picture when it comes to luxury watch awareness. Just over half of respondents listed Rolex as the luxury watch brand which came to mind first. The next closest brand – Patek Philippe – secured only 14% of mentions by comparison.

- Overall, almost three quarters (73%) said that they had purchased at least one item of fine jewellery within the past year. Meanwhile, just over half (51%) said that they had purchased at least one new luxury watch. Both figures are strongly driven by affluent/HNW Chinese.

- 43% of luxury watch/fine jewellery buyers say that they already buy these products as investments, with a further 43% open to start doing so. The affluent Chinese are particularly likely to be buying these items as investments (57%), with women and under-45s also more likely than men and over-45s to already be doing so.

- 37% of affluent/HNWIs are interested in second-hand ownership of fine jewellery and luxury watches. This rises to 45% among men and 48% in the UK. Only a quarter are interested in fine jewellery rentals, with a much higher share (36%) being not at all interested.

BRAND AWARENESS

Cartier is comfortably the most cited fine jewellery brand

Fig.1 “What is the first luxury brand which comes to mind when you think about fine jewellery?” [most selected]

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

Among the plethora of fine jewellery brands, Cartier is comfortably the most widely cited top-of-mind. 43% of the total sample listed it as the brand which came to mind first, with equally high mentions across all three countries. Tiffany is another strong performer, with almost one in five respondents listing it as the fine jewellery brand which came to mind first.

Bulgari and Van Cleef & Arpels also secured a reasonable number of mentions, while various other well-known brands such as Chanel and Pandora only gained a handful. Some other globally renowned brands such as Piaget and De Beers did not gain enough mentions to make the list, indicating that they are not currently top-of-mind for many wealthy individuals.

Rolex leads the way in luxury watches

Fig. 2 “And what is the first luxury brand coming to mind when you think about luxury watches?” [most selected]

One brand also dominates the picture when it comes to luxury watch awareness. Just over half of respondents listed Rolex as the luxury watch brand which came to mind first.

The next closest brand – Patek Philippe – secured only 14% of mentions by comparison. Cartier and Omega were the only other brands which gained more than 10 mentions, with a wide range securing a handful or fewer.

Well-known brands such as Hublot and IWC Schaffhausen fall some way back in terms of spontaneous brand awareness.

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

PURCHASING TRENDS

Jewellery and watches remained popular last year

Fig. 3 “Which of the following have you purchased within the past year, and which do you plan to purchase within the next year?”

The pandemic has led many people to reassess how they spend their money. While some of our affluent community tell us that they have shifted away from buying goods and more to experiences, it is clear that items such as jewellery and watches remain popular. These products retained their appeal last year, even at the height of the pandemic.

Overall, almost three quarters (73%) said that they had purchased at least one item of fine jewellery within the past year. This figure is strongly driven by Chinese respondents, 97% of whom said they had done so compared to 65% in the UK and 56% in the US. All types of jewellery were purchased by between 30% and 40% of respondents. Meanwhile, just over half (51%) said that they had purchased at least one new luxury watch within the past year. This figure is again strongly driven by the Chinese, 73% of whom having done so compared to around 40% in the UK and US.

Around 40% plan to buy a luxury watch and/or each of the listed fine jewellery items over the next 12 months, showing an enduring purchase intent towards luxury goods. Watches have a particularly strong rate of engagement, with only 27% of respondents having not bought a new luxury watch last year and also do not plan to do so in the year ahead. This figure rises to 40% among over-45s, whereas only 16% of affluent under-45s are disconnected with the category.

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

In-store spending strongly preferred for luxury jewellery and watches

Fig. 4 “What is your preferred way of buying luxury jewellery and watches? Please drag the slider to identify your appropriate ratio between online and in store.” [median ratios]

Base: 300 global affluent/HNWIs Source: LuxuryOpinions/Altiant

The past two years have also had a significant impact on shopping behaviours. As the pandemic spread, many shops remained closed for extended periods and even when reopening, this was done carefully and with restrictions. Many countries have now removed these restrictions entirely, but caution is still widespread and the rise in popularity of online shopping is likely to continue. Nevertheless, there is a clear customer preference for buying high-end jewellery and watches from stores in all three countries, likely due to the desire to see and try the products in question.

Luxury brands’ own stores are the most popular location

For both fine jewellery and luxury watches, all three countries show a clear preference to buy directly from brands’ own shops. Affluent Chinese consumers are particularly likely to have purchased these items in branded shops over the past year, although they are also more receptive to department stores than Brits and Americans. Under-45s are also more likely than their older counterparts to want to shop in-store. Luxury brands’ own websites are also popular sales channels, with Brits and Americans as likely to use them as they are to shop in the brands’ stores.

LUXURY WATCHES - PURCHASE CHANNELS

Fig. 6 “And where have you purchased luxury watches from within the past year?”

FINE JEWELLERY - PURCHASE CHANNELS

Fig. 5 “Where have you purchased items of fine jewellery from within the past year?”

Base: 218 UK/US/China affluent and HNWIs fine jewellery buyers Source: LuxuryOpinions/Altiant

Base: 153 UK/US/China affluent and HNWI luxury watch buyers Source: LuxuryOpinions/Altiant

Buying for self is the most popular occasion for hard luxury

Fig. 7 “For each of the following items you plan to buy next year, who do you plan to buy them for?”

Base: UK/US/China affluent and HNWIs who plan to buy selected items within the next year Source: LuxuryOpinions/Altiant

For luxury watches and all types of fine jewellery, affluent respondents are most likely to buy for themselves. This is highest for watches, where four in five do so, and rising to 89% of Brits.

Partners are the next most likely recipient, with about 40% buying luxury watches or fine jewellery pieces for their significant other. This falls to around a quarter for family members and around one in ten for those buying these items for friends.

Investing in luxury watches and fine jewellery is widespread

Fig. 8 “And which of the following options is the most relevant to you?”

Of all luxury categories, jewellery/watches are in fact the most popular investments overall, ahead of items such as minerals/stones and cryptocurrencies. Luxury watches are seen as a particularly safe investment and the returns on many brands such as Rolex have even surpassed popular commodities such as gold in recent years.

Base: 273 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

Overall, 43% of luxury watch/fine jewellery buyers say that they already buy these products as investments, with a further 43% open to start doing so. The affluent Chinese are particularly likely to be buying these items as investments (57%), with women and under-45s also more likely than men and over-45s to already be doing so.

OWNERSHIP & USAGE

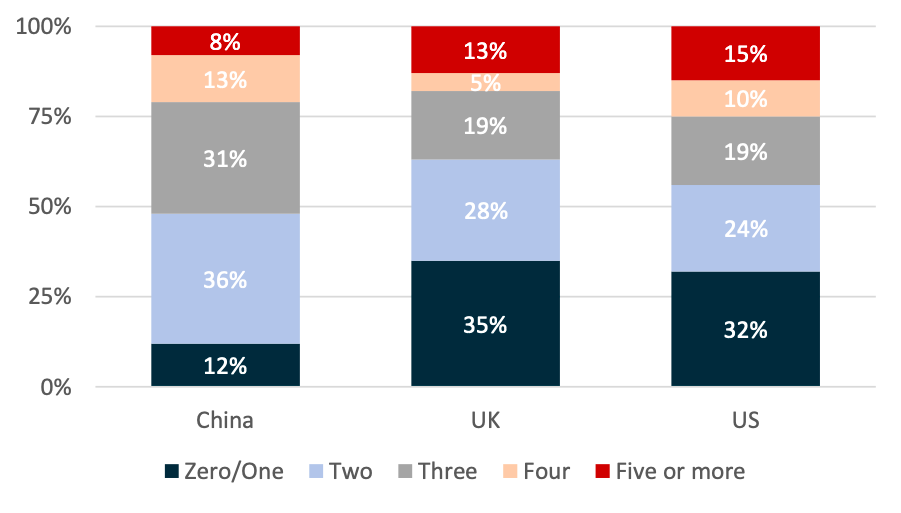

Watch ownership is high in all three countries

Fig. 9 “How many watches worth more than £1,000 (or equiv. in USD/RMB) do you currently own?”

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

Luxury watches are a popular part of many affluent individuals’ repertoire of high-end goods. These can dramatically vary in price, but for this question we used a more ‘mass affluent’ price baseline of £1,000 as this is where some luxury brands have entry-level models (e.g. Tag Heuer’s Formula 1). Overall, a quarter own zero or only one watch worth at least £1,000, although this figure rises to a third in the UK and US.

Just over a third (36%) of wealthy Chinese individuals own two luxury watches, and a further 31% own three, both being comfortably higher than for Brits and Americans. Across all three countries, around one in five say that they own four or more high-end watches. Both genders and age cohorts (under/over-45s) are equally likely to own four or more luxury watches.

More than a third wear a luxury watch every day

Fig. 10 “And how often do you wear your luxury watches?”

One of the changes arising from the pandemic has been that more people are working from home, or at least doing so more than previously. As a result, there has been a declining work-related need for formalwear and luxury goods such as jewellery and watches. Nevertheless, a third still say that they wear a luxury watch every day, rising to 44% of wealthy Chinese respondents.

The Chinese are also more likely than Brits and Americans to say that they wear them a few times a week, meaning that 78% are weekly wearers (vs 58% of Americans and 54% of Brits). Under-45s are also much more likely than over-45s to be weekly wearers of luxury watches (72% vs 53%), while women are also slightly more likely than men to do so (66% vs 61%). Brits and Americans are much more likely than the Chinese to say that they wear their luxury watches once a month or less often, or only for special occasions.

Base: 273 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

30% wear items of fine jewellery every day

Fig. 11 “How often do you wear your fine jewellery?”

Base: 273 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

As with luxury watches, three in ten say that they wear fine jewellery every day. Unlike watches however, China does not stand apart from the other two countries for daily wearers, and the US is in fact level at this frequency.

However, the Chinese are by far the most likely wearers of fine jewellery a few times a week (40%), compared to only 15% of Brits and Americans. Perhaps as expected, women are much more likely than men to wear fine jewellery at least a few times a week (68% vs 38%), with a similar pattern for under- and over-45s (67% vs 37%). As with luxury watches, those in the UK and US are much more likely to only wear fine jewellery for special occasions.

Attitudes towards Fine Jewellery and Luxury Watches

Ethical/Responsible sourcing ranks highly for affluent/HNWIs

Fig. 12 “How important to you is that any stones (e.g. diamonds) used for items such as rings are sourced responsibly or ethically?”

Responsible and ethical production has been an increasing priority for luxury brands, and this is now something which is important to most affluent/HNWIs. When it comes to sourcing of stones for jewellery pieces or watches, this relates to mining which is not exploitative to either the workers or the environment itself.

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

Overall, a quarter say that ethical/responsible sourcing of stones is essential to them, with a further 47% saying it is important. Brits and Americans show a similar level of response overall, while there is a skew towards under-45s vs over-45s (79% vs 63% respectively) for those saying that it is either essential or important to them. Only 7% of affluent/HWNIs now deem this factor as unimportant.

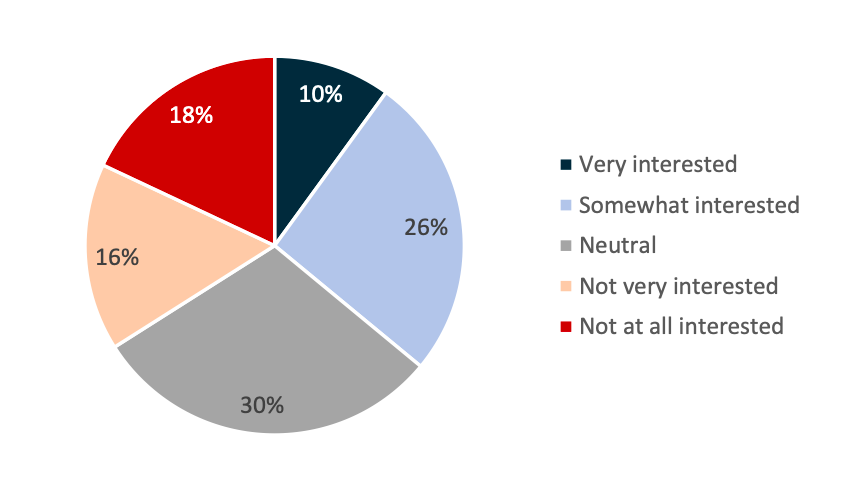

LAB GROWN DIAMONDs. A RAPIDLY GROWING SEGMENT

Fig. 13 “How interested are you in lab-grown/man-made diamonds when it comes to choosing luxury jewellery and watches?”

One of the markets which has grown rapidly to tackle issues of mineral sourcing has been that of lab-grown diamonds. These are said to be identical in appearance to mined diamonds but are of course considerably less intrusive on the environment. Consumer interest in these is currently rather mixed, with around a third of affluent/HNWIs being interested in them, a third not being interested and a third currently adopting a neutral position. Interest is highest among affluent/HNW Chinese (45%) and under-45s (42%).

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

Collaborations can ignite interest

Fig. 14 “How interested are you in collaborations between luxury and more massmarket brands (e.g. Omega and Swatch) when it comes to choosing luxury jewellery and watches?”

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

In March 2022, Omega announced a collaboration with Swatch on a more accessible version of Omega’s Speedmaster ‘Moonwatch’ priced at £207 (vs the £6,000 starting price for a Speedmaster). The launch caused a huge amount of discussion and consumer interest, so much so that Swatch had to quickly close some of its stores due to the overwhelming demand. The lower price point provided a much more accessible entry into Omega ownership, but also appealed to wealthy individuals.

Respondent interest bears this out: 51% say they are interested in collaborations such as these, albeit with the response heavily driven by China (83%). Overall, a quarter say they are not very/not at all interested in such collaborations, with Brits and Americans being more circumspect and perhaps more likely to judge on a case-by-case basis.

Second-hand more likely to generate interest than rentals

Fig. 15 “How interested are you in buying second-hand and renting when it comes to choosing luxury jewellery and watches?”

The popularity of second-hand platforms has gathered momentum over the past few years, with increasing numbers of people looking to declutter their lives and actually own fewer products in general. Second-hand and rental platforms such as Vestiaire Collective and Rent the Runway look to appeal to those who are more attracted to more ‘transitory’ ownership, but also consumers who want to experience a brand which they might not be able to otherwise.

Base: 300 UK/US/China affluent and HNWIs. Source: LuxuryOpinions/Altiant

Specifically to luxury jewellery and watches, 37% of affluent/HNWIs are interested in second-hand ownership. This rises to 45% among men and 48% in the UK. Just over a third of the sample say that they are currently not interested in buying these luxury items second-hand. Unusually for the affluent Chinese consumer, who is often enthusiastic towards new market developments, only a quarter are interested in buying second-hand. Conversely, Chinese affluent/HNWIs are the most likely of the three regions to be interested in renting luxury jewellery or watches, albeit at only 31%.

Overall, only a quarter are interested in fine jewellery rentals, with a much higher share (36%) being not at all interested. Under-45s are also more likely than over-45s to be drawn to doing so (30% vs 17%). One possible reason for the slower growth of rental jewellery and watches may lie in the fact that many wealthy individuals see them as good investments to own (see Fig. 8). Alternately, 54% say that they wear their fine jewellery at least a few times a week, while 64% do so for watches (see Figs. 10 and 11). It is likely that a rental mechanism will have limited appeal to people such as this.

This short report is intended to provide an up-to-date snapshot on some of the key trends in the hard luxury market in 2022. Our next category report will look at luxury automotive and will publish within the next month (June 2022). For more information on this study or any other research requirements, please contact us at reports@altiant.com.

To view the data set in full, or speak to us about any of your luxury research requirements, please email us at contact@altiant.com

Contributors

Chris Wisson, Knowledge Director

Viktoria Prazova, Senior Project Manager

Contact

reports@altiant.com

media@altiant.com

Publications contained in the Altiant Knowledge Center are free to use, we simply require proper attribution. In no event shall Altiant be liable for any indirect, special or consequential damages in connection with any use of the provided data. Altiant does prohibit the selling of any information contained within or derived from these reports and monitors.