Global Luxury AND ASSET MANAGEMENT (GLAM) MONITOR

sentiments and behavioUrs of the world’s affluent and high net worth populations

THE LUXURY CONSUMER’S MINDSET

Q3 2020 EDITION

DEFINING LUXURY: THE LUXURY CONSUMER’S MINDSET

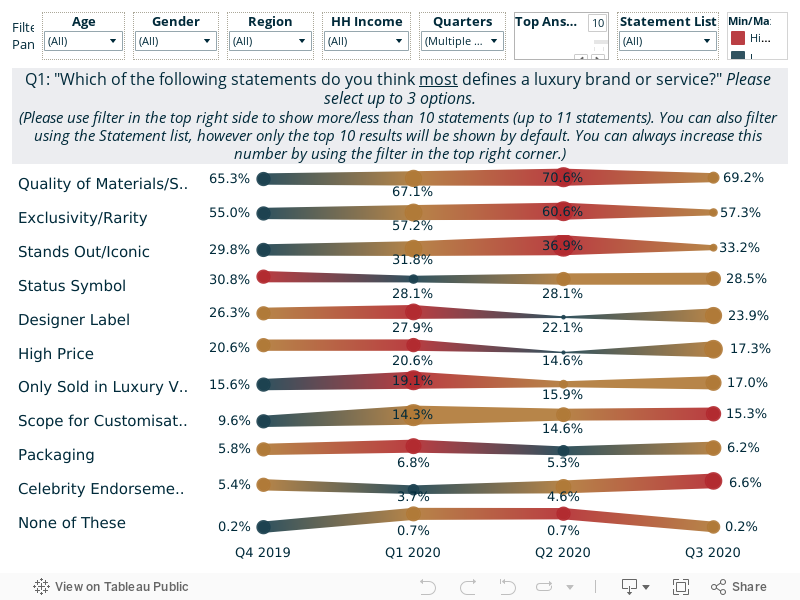

There continues to be little quarterly variance in how affluent/HNW respondents define luxury brands and services. Quality and exclusivity comfortably remain the most meaningful factors, cited by 69% and 57% respectively in Q3. All other factors are cited less often, securing around a third or less of respondents’ answers, such as 33% identifying luxury brands as standing out/being iconic.

It is clear that many consumers define luxury on grounds other than just price, with only 17% associating luxury with an elevated price. Similarly, only 24% cited a designer label as a luxury indicator, a fairly small but evident fall against pre-Covid levels. Whether this is a consequence of many affluent consumers’ scrutiny of their finances post-Covid will become clearer in the coming quarters. A minority of affluent/HNWIs continue to cite only being sold in luxury venues (17%), scope for customisation (15%), celebrity endorsements (7%) and packaging (6%) as links to luxury.

Looking across all quarters, 18-39s are more likely than over-40s to define luxury brands on grounds of higher prices and status symbols, whereas older consumers are more likely to do so based on exclusivity/rarity and high quality. Meanwhile, men remain much more likely to define luxury as being a status symbol, but are less likely to do on so based on having high prices and designer labels.

Results across the three regions also show stark variance. Across all quarters, Americans are the most likely to define luxury by the quality of materials/service, designer labels and standing out/being iconic. Meanwhile, Asians are most likely to identify with status symbols, high prices and celebrity endorsements, and Europeans to do so on grounds of exclusivity/rarity.

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/AltiantTHE LUXURY CONSUMER’S MINDSET: SPENDING ATTITUDE 1/2

Despite their typically high levels of wealth, the spread of Covid-19 has negatively impacted many individuals and led them to reassess their luxury purchases. Altiant’s recent Covid-19 tracking study found that in the third wave of data (June 2020), between a third and half of affluent/HNWIs in France, UK, US and China reported a negative financial impact (see Covid report here).

Nevertheless, there was evidence of a surprising uptick in the share of respondents saying that money is no objectto them. Despite only rising slightly in Q3 2020, this brought the total to 24%, the highest point across all quarters of study to date. 18-39s (31%), women (28%) and Asians (34%) are the clear drivers of this trend and suggests that these groups may be the most carefree spenders in the coming months. The fact that Americans were the most likely to cite this in Q2 reflects the differing timescales of Covid’s proliferation and the fact that some wealthy Chinese individuals are now adopting a ‘revenge spending’ mentality.

Half of our sample in the last quarter say that they only occasionally spoil themselves, with Americans the most likely to respond here (59%) along with over-40s (52%). With many wealthy individuals likely to remain financially conservative in the coming months, luxury purchases will often remain considered rather than impulsive in nature. Americans are also by far the least likely to stick to a budget, only 7% doing so versus 18% among Europeans and 17% of Asians (14% average). Europeans are the most likely to be bargain hunters, 17% doing so against the Q3 average of 12%.

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/AltiantTHE LUXURY CONSUMER’S MINDSET: SPENDING ATTITUDE 2/2

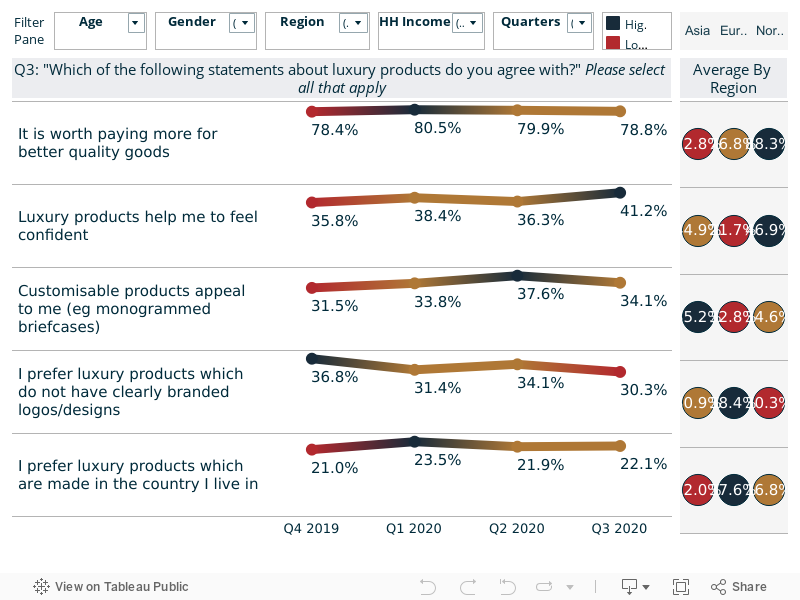

The spread of Coronavirus has had an impact on many people’s interactions with both luxury and mass-market goods and services. Nevertheless, luxury goods remain popular and still have a cachet with our affluent panel. Across all quarters of the study so far, four in five agree that it is worth paying more for better quality goods, standing at 79%in Q3. This figure rises to 89% among American respondents, 84% among over-40s and 82% among men.

Meanwhile, 41% of the Q3 sample say that luxury goods help them to feel confident, a figure strongly driven by Americans and Asians but falling to just 25% of Europeans. Under-40s (49%) are also much more likely than over-40s (35%) to gain confidence from luxury goods. Instead, Europeans continue to be comfortably the most likely region to prefer luxury products from their home country (37% vs 22% average), falling to just 12% of Asians, the latter figure highlighting the ongoing appeal of Western products and services for these consumers.

Europeans are also the most likely of the three regions to prefer luxury products which do not have clearly branded logos or designs (37% vs 30% average). 30% reflects the lowest point across all quarters of study so far, suggesting that discretion is becoming a preference for more wealthy consumers. Finally, customisable products appeal to 34%of the Q3 sample, a figure driven by under-40s and women (43% and 39% respectively).

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/Altiant

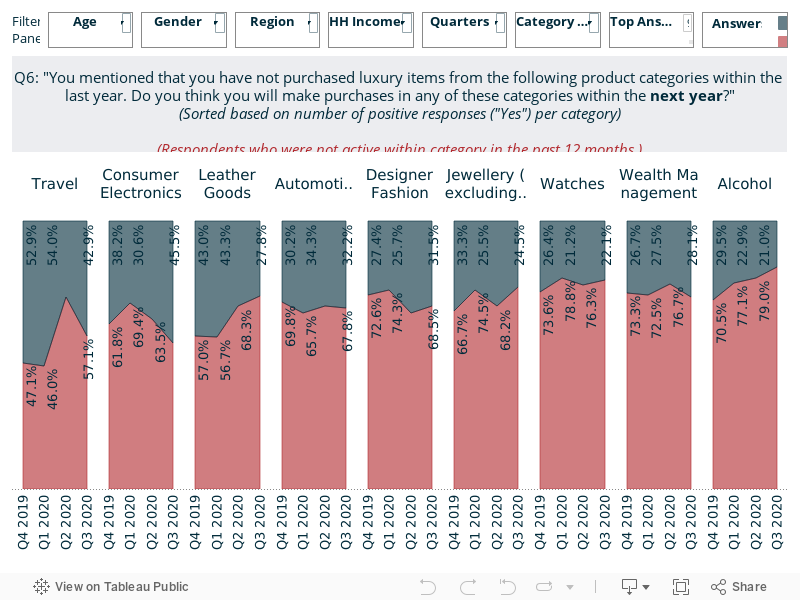

THE LUXURY CONSUMER’S MINDSET: Luxury purchases (Past 12 Months)

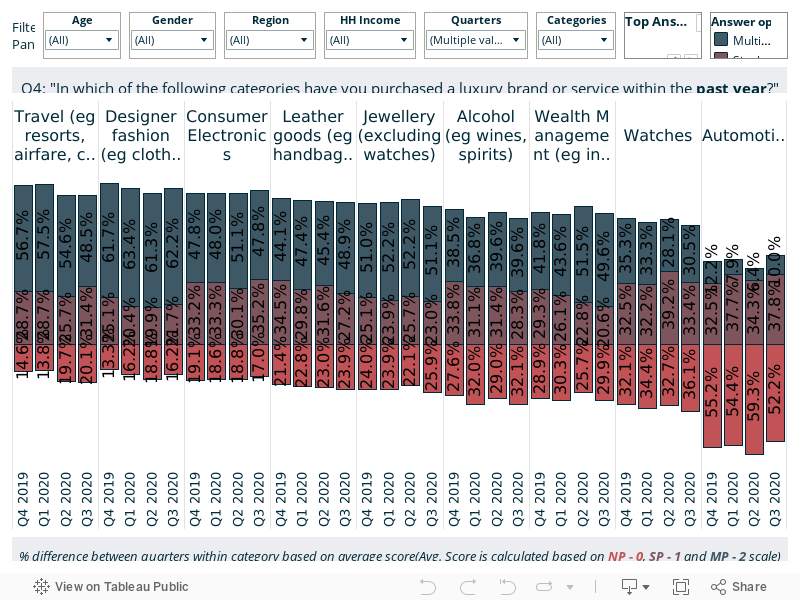

Before 2020, travel numbers previously saw little quarterly variation in our tracking study, reflecting the all-year-round appeal and/or necessity of luxury travel. However, travel has been one of the hardest hit categories by Covid-19, with international holidays largely prohibited in Q2. While some countries reopened their borders to holiday-goers in Q3, many wealthy individuals have remained cautious and eschewed international trips, especially those which are longer-haul. This is likely to continue in the coming quarters until faster testing and/or a vaccine can give greater confidence to travellers.

Some 80% of our Q3 2020 sample said that they had taken a luxury holiday within the past year, and 49% did so multiple times. However, these represent dips from pre-Covid results, reflecting the downturn in travel for this year. Of the three regions, Europeans are the least prolific travellers, 34% of Europeans still took multiple holidays as per the Q3 results, though this rises to 51% of Americans and 59% of Asians.

Pre-2020, designer fashion trailed a short distance behind tourism for purchasing penetration. However, fashion has forged ahead of tourism in 2020, with many consumers shifting their purchases online. In Q3, 84% said that they had bought a high-end fashion item within the past year, with 62% making multiple purchases. High-end electronics (83%), leather goods (76%) and alcohol (74%) have also remained widely popular in 2020, with under-40s and Americans the most likely to make multiple purchases in all three of these categories. Designer fashion, leather goods and jewellery also see a clear skew in purchases towards women.

Luxury automotive is comfortably the least likely category to be purchased (48%), a reflection on the higher cost and infrequent necessity of buying new cars. Furthermore, 34% expect to cut back on category spending in the year ahead, the second most likely category to see a cutback (after travel). With Coronavirus meaning that many people are spending more time at home for both work and leisure, some households may have less need for several cars.

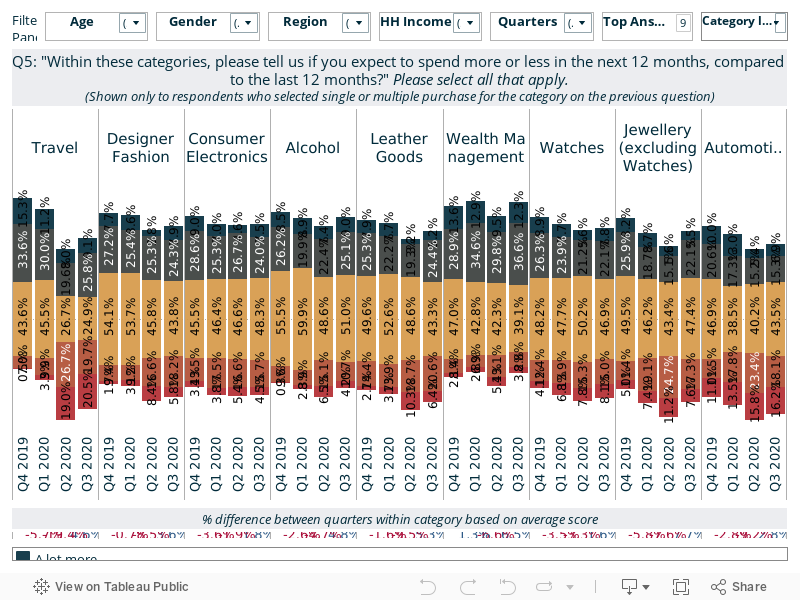

Elsewhere, planned purchasing trends for 2020 look a little less positive as many affluent consumers expect to cut back on their luxury purchases in response to Covid-19. Jewellery may be well placed to bounce back from Covid, with only 25% of jewellery buyers in Q3 sample expecting to spend less in the year ahead, 11 percentage points lower than in Q2 and returning the result to pre-Covid levels. Over the past two quarters, leather goods, designer fashion, alcohol and wealth management have seen clear increases in the share of respondents expecting to reduce their purchases in the year ahead.

Unsurprisingly, travel was the worst performer, 40% expecting to reduce their travel spending in the year ahead compared to 13% in Q1. However, that this is down from 46% last quarter may indicate cautious confidence in travelling returning. Similarly, 35% expected to increase their travel spending for the year ahead in Q3, up from 28% in the previous quarter. Wealth management also saw a clear bounce back in Q3, with 49% expecting to spend more, up from 39% in Q2. This may suggest that some wealthy individuals are seeing investments as a good way to manage their money while there remains uncertainty about Covid’s ongoing impact.

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/AltiantTHE LUXURY CONSUMER’S MINDSET: Luxury Purchase Intent (Active Past 12 Months)

Among non-users in the different categories, automotive is the most likely to be unable to entice new customers in 2020. 36% of non-users do not expect to buy a car in 2020, although 17% did expect to buy a new car in the year ahead. Just under a quarter of current non-buyers of jewellery, wealth management and watches said that they would enter these categories within the next year.

Back to Top

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/AltiantTHE LUXURY CONSUMER’S MINDSET: Luxury Purchase Intent (Inactive Past 12 Months)

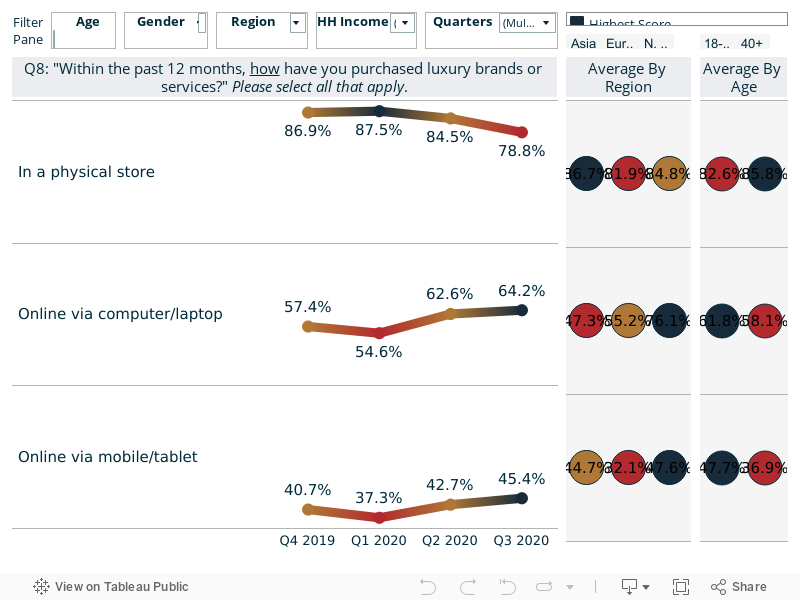

Unfiltered Base: 3,069 global affluent/HNWIs | Source: LuxuryOpinions/AltiantTHE LUXURY CONSUMER’S MINDSET: Purchase Channels

The Coronavirus outbreak will continue to fundamentally influence how shoppers buy products and services. Many stores were closed throughout spring and early summer, only opening in earnest since June across the world. Social distancing and face masks are now compulsory in shops in most countries, though many affluent consumers remain wary of face-to-face interactions and have shifted more of their shopping online.

The share of consumers buying luxury goods/services in a physical store within the past 12 months remained around 85% over the previous study quarters. However, we are now seeing the evidence of the aforementioned shift in shopping habits, with 79% saying they had shopped for luxury goods in a store. While this remains a high number, we anticipate further erosion of this number until a vaccine for Covid-19 is available to enable some consumers to feel more comfortable about shopping in person (see The Post Covid Luxury Consumer).

In turn, the past two quarters have seen a significant uplift in the share of respondents buying luxury goods online. In Q3 2020, 64% reported to buying luxury goods and services online via a computer/laptop within the past year, while 45% did so via their mobile phone/tablet. Both of these represented significant increases over the previous quarter and reflect many affluent shoppers’ current preference for the safety of online purchases. Indeed, the figure for mobile phone/tablet purchases is the highest across all study quarters so far, a figure which we expect to continue nudging upwards in the coming quarters.

Over-40s, males and Americans are the most likely to prefer online shopping via computers/laptops as per the Q3 data, whereas under-40s, women and Asians are the more likely mobile/tablet shoppers. As many shoppers continue to stay away from stores over the coming months, it will become increasingly important for brands to deliver reliable and user-friendly online platforms, particularly when it comes to providing clear resolutions on smaller screen devices.

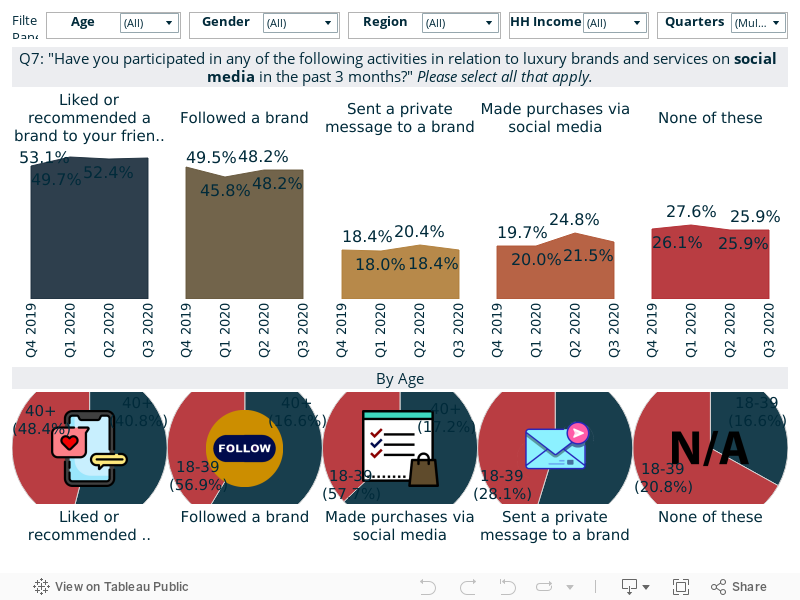

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/AltiantTHE LUXURY CONSUMER’S MINDSET: Social Media Interactions

In line with the growing popularity of online retailing, social media has also become more important for many luxury brands. Creating engaging and relatable content proved to be a lucrative sales channel for brands while individuals were in lockdown. The popularity of TikTok in particular over the past few months has attracted a growing number of luxury brands to this app.

Social media engagement and interactions have showed minimal quarterly variations across the tracker so far. 53% of our Q3 sample said that they had liked or recommended a brand to family, friends or colleagues. Many brands have responded to the Covid-19 outbreak with altruistic messages and actions, which may be related to the small upturn in recommendations in 2020. Meanwhile, the share of respondents following a brand (48%) and sending a private message to a brand on social media (18%) remained broadly flat against Q2.

Q2 saw a clear uptick in the share of consumers making purchases via social media, rising to 25%. Enforced lockdown measures was the likely reason for this as many consumers had more time to explore social media channels and purchase from brands at leisure. This number fell back to 22% in Q3, a likely reflection of lockdown restrictions easing. Women (30%) and under-40s (29%) are much more likely than over-40s and men to make luxury purchases via social media.

Unfiltered Base: 4,120 global affluent/HNWIs | Source: LuxuryOpinions/AltiantAll data presented in this GLAM monitor has been sourced from Altiant’s manually validated in-house panel of Affluent and High Net Worth Individuals (HNWIs), Luxury Opinions©. This iteration reports on Q3 2019 but will also include trended data from the four previous quarters. In order to protect data integrity, all respondents can only answer the survey once a year at most. For any additional questions about this research, please contact glam@altiant.com.

Publications contained in the Altiant Knowledge Center are free to use, we simply require proper attribution. In no event shall Altiant be liable for any indirect, special or consequential damages in connection with any use of the provided data. Altiant does prohibit the selling of any information contained within or derived from these reports and monitors.